When Tax Returns Don’t Tell the Whole Story…

There’s Another Way to Get Approved for a Home Loan

Self-employed, commission-based, or variable income?

You may qualify using methods most banks don’t offer.

Why Traditional Mortgage Lenders Say No — Even When Your Income Is Strong

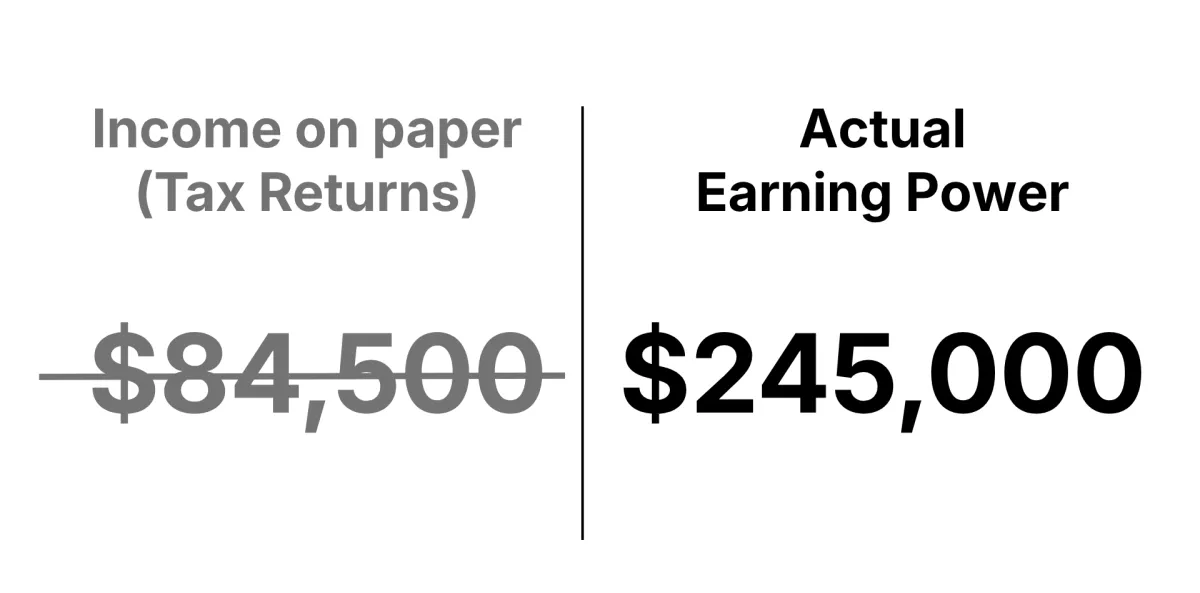

You did exactly what your CPA advised.

You minimized taxes and kept more of your income.

But to a traditional bank or lender… that works against you.

Their systems rely heavily on tax returns —

often ignoring your actual cash flow, revenue, and earning power.

The Income Reality Gap

There’s a smarter way to evaluate income — and it changes everything.

I Don’t Use One Formula to Approve You.

As an independent mortgage broker with access to 300+ lenders through NEXA Lending,

I’m not limited to one set of guidelines. I match your situation to the right solution.

Income Beyond Tax Returns

Modern income evaluation methods — for 1099 & self-employed borrowers as well as W2 employees — that reflect what you actually earn.

Using Your Assets To Qualify

Your savings, investments, and overall financial strength can be used to qualify — without forcing everything through traditional income formulas.

Using Rental & Investment Income

Rental properties and investment income can be used to qualify — even when traditional lenders won’t count it properly.

Real Examples of How Borrowers Are Getting Approved

Every scenario is different — we use the right method to evaluate your income.

These approaches can be applied to both purchases and refinances.

Self-Employed Contractor, L.A.

Problem:

Denied by a traditional bank due to low taxable income after write-offs.

Solution:

Instead of tax returns, income was evaluated using 12 months' bank deposits to reflect real cash flow.

Result:

Approved based on business revenue trends — not reduced net income on taxes.

Real Estate Agent, Orange County

Problem:

Strong commissions, but heavy write-offs lowered qualifying income on tax returns.

Solution:

Qualified using 1099 only income, without relying on adjusted taxable income.

Result:

Approved based on gross earning ability and consistency — not post-deduction income.

Business Owner, San Diego

Problem:

Tax returns didn’t accurately reflect true income due to reinvestment and deductions.

Solution:

Used a 12-month Profit & Loss (P&L) statement to show actual earnings.

Result:

Approved using real business performance instead of tax-reported income.

W2-Employed Nurse, L.A.

Problem:

Year-to-date income appeared lower due to fluctuating overtime and shift changes.

Solution:

Underwriting focused on prior-year W2-only income (no paystubs) instead of inconsistent current-year averages.

Result:

Approved using a more accurate representation of earning capacity.

Property Investor, Riverside

Problem:

Multiple properties created heavy write-offs, reducing taxable income.

Solution:

Qualified using rental income from the property itself (Debt Service Coverage Ratio) — no personal income required.

Result:

Approved based solely on property cash flow, not personal tax returns. In many cases, no lease agreement is required.

Retiree, San Bernardino

Problem:

No regular documentable monthly income aside from Social Security which was insufficient on its own.

Solution:

Assets were converted into a calculated income stream (asset depletion method).

Result:

Approved using both SS benefits + wealth and reserves instead of employment income.

Still not seeing a path that fits your situation? There are additional options — including programs that don’t require income or employment verification.

The next step is figuring out which approach works for your situation.

Let’s Look Beyond Your Tax Returns

We’ll evaluate your income the way traditional mortgage lenders don't — and show you what's actually possible.

15-minute call. No pressure. Just clarity.

NMLS #1064307 | Equal Housing Opportunity

All loans subject to underwriter approval. Terms and conditions apply. This is not a commitment to lend. Mitch Chang Mortgage is a licensed mortgage broker in California. Complex income scenarios require individualized review.

Licensed in CA, HI

Contact Us 📞 562-667-4832 ✉️ [email protected]

© 2026 Mitch Chang Mortgage. All rights reserved. | Privacy Policy | Terms of Service